Fund accounting versus traditional accounting for nonprofits

.svg)

.svg)

.svg)

.svg)

Most nonprofit leaders start their careers thinking about impact, not accounting systems.

But sooner or later, a grant agreement, an audit request or a frustrated donor asks a question that standard bookkeeping can't answer. Suddenly, the gap between how money has been tracked and how it’s supposed to be tracked becomes very clear.

Fund accounting fills that gap. Here's what you need to know.

What is traditional accounting? Why might it fall short?

Traditional accounting tracks money in and money out with one goal: measuring profitability. The model works well for businesses, but wasn't designed for organizations that exist to advance a cause rather than generate a return.

Standard bookkeeping handles basic transaction recording, cash flow tracking and general financial reporting. This is what most small organizations start with.

When traditional accounting isn’t enough for nonprofits

For a small, for-profit business, traditional accounting might be enough. However, for a nonprofit, it quickly becomes a problem.

Donors, grant makers and the IRS don't just want to know how much money came in. They want to know where specific dollars went, how restricted funds were spent and whether financial reports can prove it. Traditional accounting systems weren't built to answer those questions.

What is fund accounting?

Fund accounting is a system that organizes money by its designated purpose, versus tracking it as a single pool of resources. It is the standard accounting method for nonprofits because donors, grantmakers, auditors and the IRS all require organizations to show that money was spent as intended.

Traditional accounting asks, "Did we make money?"

Fund accounting asks, "Did we use the money the way we promised?"

This shift in question reflects a shift in purpose: nonprofits are accountable to their funders, not optimizing for profit.

What fund accounting looks like

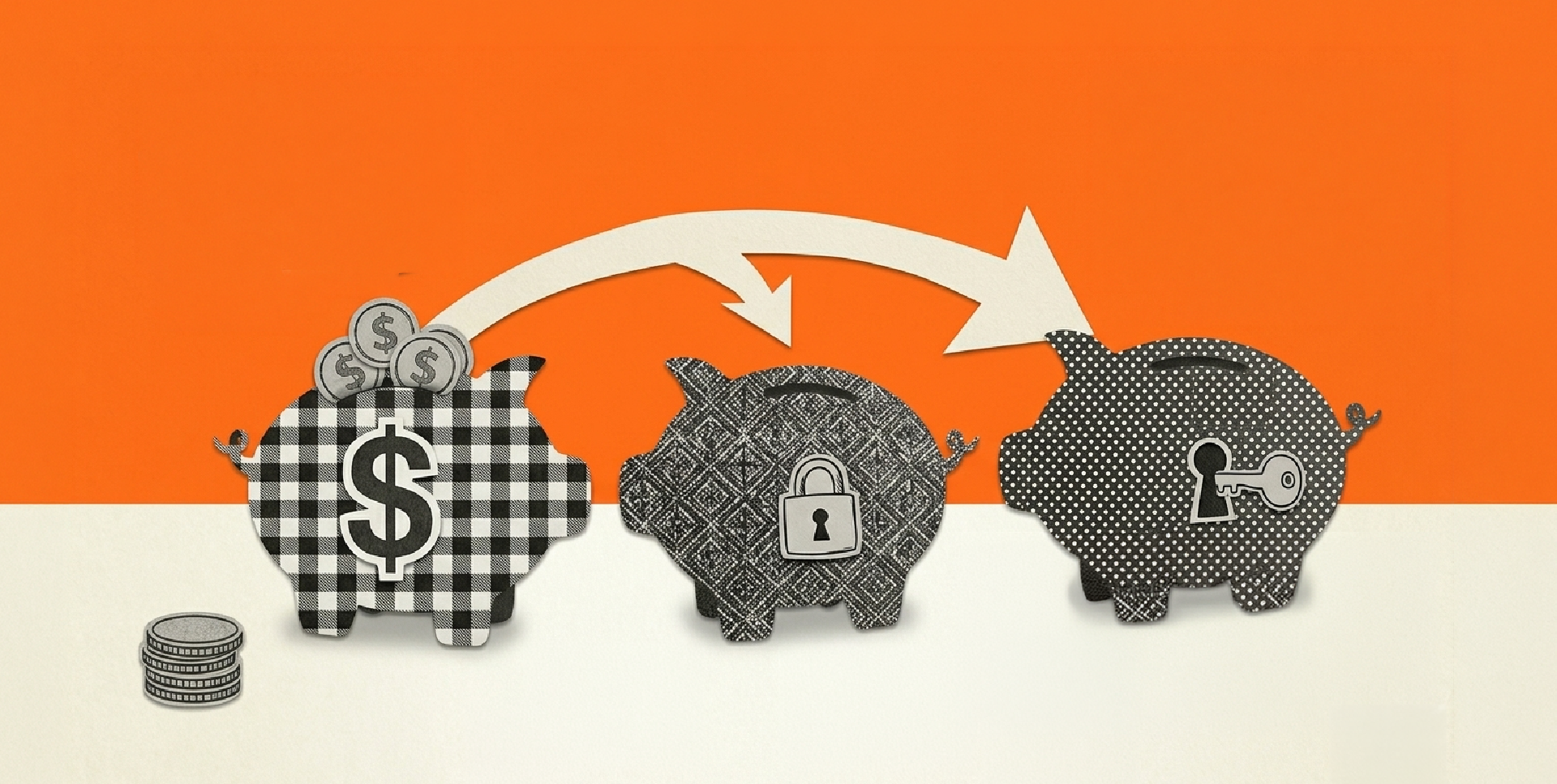

In practice, fund accounting organizes money into separate "funds," each one a regulated unit with its own balance, restrictions and reporting obligations. Each fund is like a labeled piggybank: tracked independently and governed by its own rules about how the contents can be spent.

This structure is especially practical since grantmakers build it into their agreements, auditors look for it in financial statements and the IRS requires it on Form 990, the annual nonprofit tax filing form on which expenses are detailed according to functional category.

.jpg)

Fund accounting vs. traditional accounting: what’s the real difference?

Fund accounting and traditional accounting answer different questions, serve different stakeholders and produce financial reports that look nothing alike. Here are the major distinctions.

- Primary purpose: Traditional accounting measures profit. Fund accounting proves that every dollar was spent as intended for the benefit of donors, grantmakers and the public.

- Financial structure: Traditional accounting uses a single general ledger. Fund accounting splits it into multiple regulated funds, each with its own income, expenses and balance. Money can’t flow from one fund to another without a formal transfer and documentation.

- Key financial reports: For-profit businesses produce an income statement and a balance sheet. Nonprofits produce a Statement of Activities, a Statement of Financial Position and a Statement of Functional Expenses, which break spending into program services, management and fundraising.

- Resource flexibility: Business revenue is generally unrestricted. Nonprofit revenue often is not, with a single organization likely to manage unrestricted funds, restricted grants and temporarily restricted donations simultaneously, each pot with its own rules about how and when it can be spent.

- Principal stakeholders: Traditional accounting answers to shareholders seeking a financial return. Fund accounting answers to donors, grantors and the public, and shows proof the mission is being funded as promised.

.jpg)

What are the three fund types nonprofits need to understand?

Most nonprofit fund accounting is built around three core fund categories, each governed by distinct rules about how the money can be used.

Under FASB's ASU 2016-14 standard, these categories are formally reported under two classes: net assets without donor restrictions and net assets with donor restrictions. (Note that before 2018, the categories were listed as unrestricted, temporarily restricted and permanently restricted.)

The leading fund types on compliant financial statements include:

- Net assets without donor restrictions (formerly "unrestricted"): These are the most flexible resources a nonprofit organization holds. Funds in this category carry no donor-imposed limitations and can be directed toward operations, staff costs, overhead or any other organizational need.

- Net assets with donor restrictions – time- or purpose-bound (formerly "temporarily restricted"): These funds come with conditions attached, either a time restriction (funds to be used by a certain date) or a purpose restriction (funds designated for a specific program or project). The restriction lifts once the condition is met, at which point the funds move into the without-donor-restrictions category.

- Net assets with donor restrictions – perpetual (formerly "permanently restricted"): The principal value of a perpetually restricted fund remains intact indefinitely. Only the investment earnings generated by that principal are typically available to spend, and often only for a specific purpose designated by the donor.

When does a nonprofit actually need fund accounting?

A full fund accounting system isn’t essential on day one, but it becomes advantageous if an organization:

- Receives grants with specific spending obligations

- Manages multiple programs with separate budgets

- Prepares for an independent financial audit

Filing a Form 990 with functional expense categories is another clear trigger, as is a growing donor base that expects financial transparency. Each of these situations involves accountability that a single general ledger can't reliably satisfy.

Make tracking donations easy with Give Lively

Nonprofit fund accounting only works when the donation data flowing into it is clean, organized and traceable back to its source. That's where a nonprofit fundraising platform matters.

The Give Lively fundraising platform, which is free for nonprofits, delivers detailed, campaign-level donation data in real time, on-demand data exports and integrations with both Salesforce (direct sync) and Zapier (for automated workflows to other customer relationship management programs). These features, along with others, ensure that relevant records are ready when it's time to reconcile.

Learn more about Give Lively’s nonprofit fundraising platform today.